Opens in new window

Opens in new windowUp until the early 2020s, global trade revolved around the relationship between the US and China. In recent years, geopolitical tensions and market shifts, coupled with a change in sourcing economics, have caused a shift in this dynamic, resulting in a “multi-polar” structure where more countries participate in global trade.

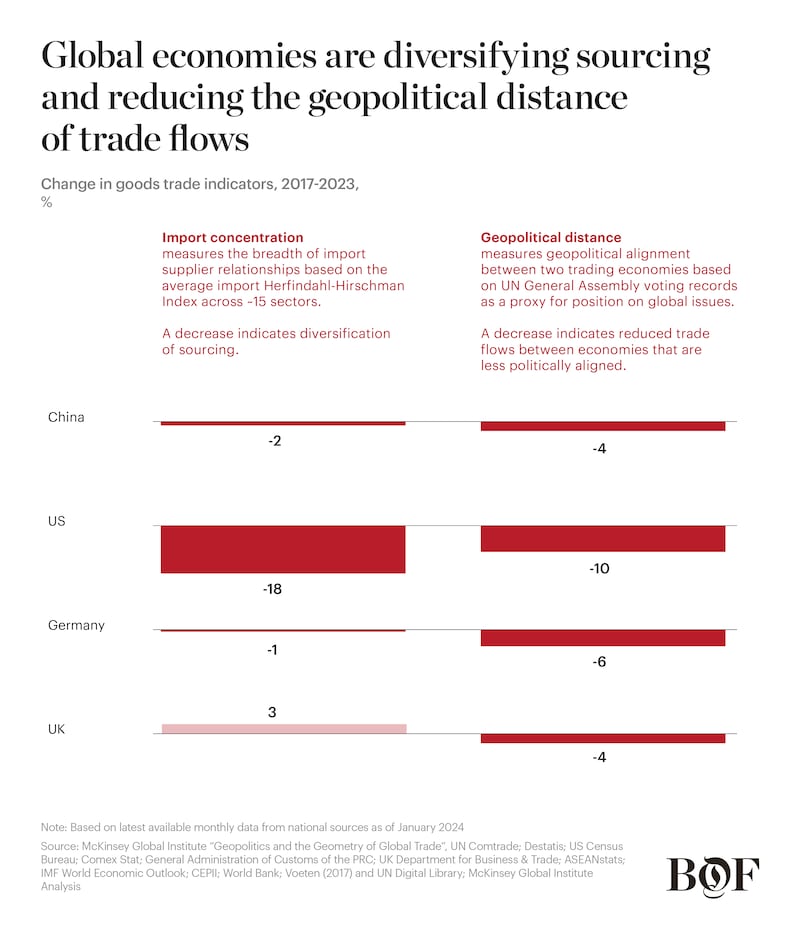

This push to diversify trade flows is happening across industries. Between 2017 and 2023, the share of total US imports from China fell by 5.8 percentage points, with imports in strategic industries such as electronics reducing by more than 20 percent in 2023. In the same year, the EU cut the overall trade deficit with China by 27 percent to diversify supply chains in strategic industries such as electronics and chemicals.

In parallel, other major economies are also reducing risk by trading with more geopolitically aligned countries. These economies, predominantly China, Germany, the UK and the US, have reduced the geopolitical distance of their trade by 4 to 10 percent in the last five years.

In The State of Fashion 2025, BoF and McKinsey explain how these shifts will impact fashion companies in the year ahead, outlining the moves that executives should make to build more resilient supply chains.

Diversification of apparel and textiles sourcing will likely continue at pace in the years to come

Players are increasingly diversifying their sourcing footprint to create supply chain resilience. The share of apparel and textiles coming from China decreased by 6 percentage points between 2019 and 2023 for the US and 3 percentage points for the EU. The total value of imports from China declined by 5 percent on average per year during this period, compared to a less than 1 percent average yearly decline in the previous decade for the US. Similarly, for the EU, the total value of imports declined by 2 percent on average per year, compared to a 1 percent average yearly decline in the previous decade.

Markets such as India, Vietnam and Bangladesh are expected to become key sourcing hubs for US and European apparel and textiles. Meanwhile, China is progressively losing cost-competitiveness due to rising labour costs, which increased by 38 percent from 2010 to 2021.

Nearshoring is expected to become an increasingly relevant sourcing strategy, with US and EU apparel and textile imports from nearshoring destinations expected to increase 2 percentage points and 3 percentage points respectively by 2030.

Rising sourcing costs, tariffs and sustainability targets may accelerate sourcing diversification

165%

— increase in Asia-to-US shipping costs between Dec. 2023 and Feb. 2024 due to logistics disruptions

The economic and geographic advantages of sourcing regions are shifting, with several emerging markets becoming more cost-competitive due to several factors.

Increasing labour costs in China are compromising manufacturer cost-competitiveness compared to other Southeast Asian countries such as Vietnam, where average hourly labour costs are less than half of those in China.

Shipping costs have drastically increased across Asia-to-US shipping routes. There was a 165 percent increase in Asia-to-US east coast route container rates on Feb. 05, 2024, compared to two months prior. Meanwhile, shipping prices across trade routes in the Middle East have increased 5x from December 2023 to February 2024.

5x

— increase in the number of trade restrictions since 2015, with ~3,000 imposed in 2023

Mentions of “tariffs” and “trade policies” across apparel company reports and investor presentations have increased by more than 50 percent since 2020.

As of May 2023, the EU is planning to impose import duties on goods under €150 ($164) from China, impacting an estimated 2.3 billion items per year. Southeast Asian countries are also restricting Chinese imports, with tariffs of up to 200 percent on imported textiles. The US is considering excluding Chinese imports from its de minimis import rule, where goods valued at less than $800 are duty free.

63%

— share of fashion brands that need to accelerate emission reduction efforts to reach 2030 targets

Changes in country of production alone can heavily influence greenhouse gas emissions. There is wide emissions variance between suppliers, given more than 70 percent of fashion industry emissions come from upstream activities, primarily textile production.

For example, Pakistan has half the emissions factor in fabric production than China, due to a lower share of coal-based energy production. As a result, some fashion companies have started to invest in the decarbonisation of their footprint, such as H&M’s investment in Bangladesh Wind Power in 2024.

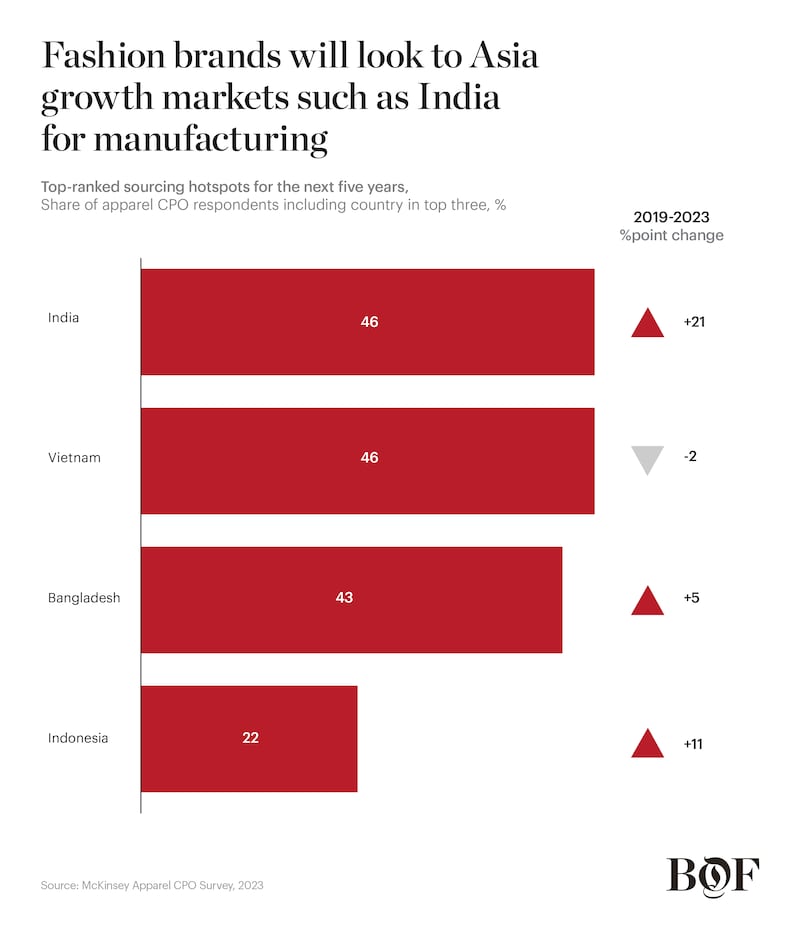

Fashion brands will look to Asia growth markets such as India for manufacturing

Fashion brands initially turned to Vietnam to reduce their dependency on China, with the value of apparel and textile exports from Vietnam increasing 35 percent between 2015 and 2020. Now, other Asian countries such as India and Bangladesh are also hotspots. In the US, apparel and textile imports from these countries increased 3 percentage points and 2 percentage points respectively between 2020 and 2023. This trend is expected to continue as fashion executives rank Asia growth markets as their top sourcing hotspots for the next five years and regulatory incentives fuel manufacturer capability building in these countries.

India is expected to play a more prominent role. While challenges in production capabilities have impacted scale to date — India had the highest percentage of apparel products that failed quality standards in 2023 — these pressures may start to ease. The Indian government has invested around $2.5 billion in Production-Linked-Incentives and reforms to Quality Control Orders, while foreign investment has increased 3x since 2019.

Bangladesh, despite being a favoured sourcing location in recent years, has experienced increased political and climate disruptions, leading to brands shifting up to 40 percent of orders in the second half of 2024 to other markets in the region.

Renewed interest in nearshoring is leading to increased capacity and improved capabilities

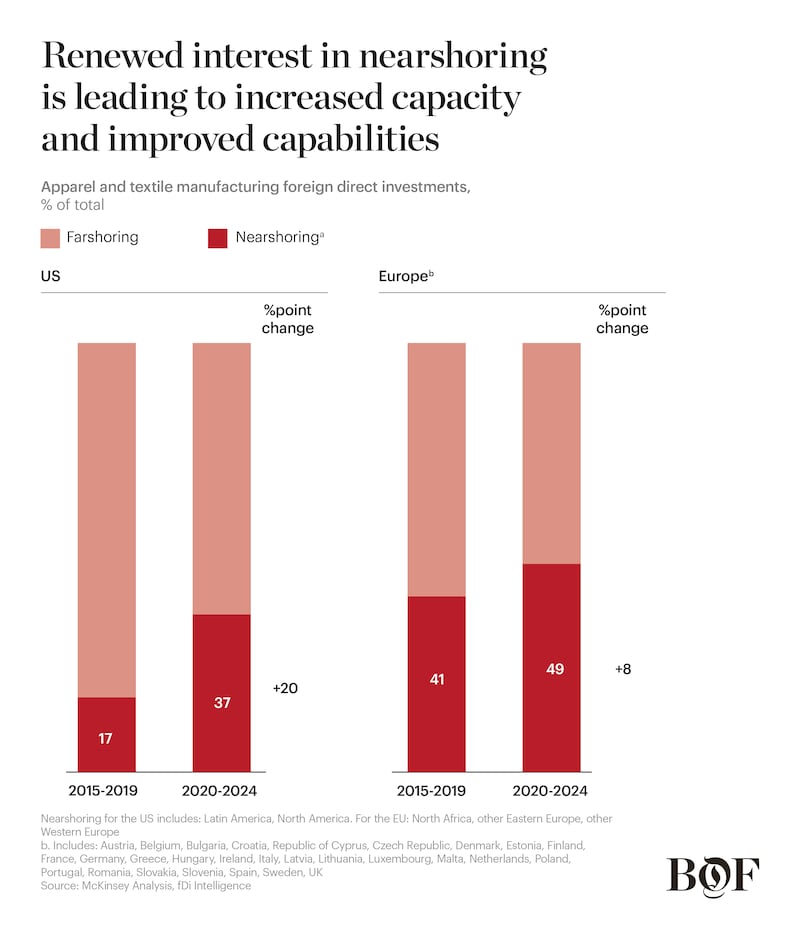

While mentions of nearshoring in corporate presentations increased 20-fold between 2018 and 2022, the share of imports to Europe and the US from nearshoring countries has remained flat since 2019. This is due to the limited manufacturing capacity and capabilities of local suppliers, with lower labour productivity meaning total landed cost remains higher than other regions — despite competitive labour rates, lower shipping costs and tariff advantages. However, these challenges are likely to be addressed going forward.

Capacity and capability building

- Investments: The share of apparel foreign direct investment into nearshoring manufacturing has increased by 20 percentage points for the US and 8 percentage points for Europe in the last five years.

- Government incentives: The Americas Act — a bipartisan bill in the US — if enacted would dedicate $14 billion to apparel subsidies and investments in nearshoring. The EU Strategy for Sustainable Textiles laid out several initiatives to reduce environmental impact in 2023, which may be addressed through nearshoring.

Cost-competitiveness

- Productivity: Local manufacturers and Asian companies with facilities in Central America are investing in vertical integration of textile manufacturing and fabric supply to improve productivity, while China’s shifting workforce demographics are causing its productivity advantage to slowly decline.

- Speed to market: As the pace of trend cycles accelerates, nearshoring could benefit company bottom lines by potentially leading to 3-5x faster lead times, higher net margins and lower inventory levels.

Latin America is emerging as a key nearshoring hub for the US, as is Turkey for Europe

65 percent of US fashion companies say they increased sourcing from USMCA members in 2023, especially Mexico — up from 40 percent in 2020 — owing to advantageous trade agreements for textiles and apparel and increased US investments.

Mexico-US shipping routes have cost and speed advantages compared to China, costing around $5,000 for a single container vs $18,000 and taking 5-10 days vs 60 days in China, the latter of which has doubled due to supply chain disruptions.

The value of apparel and textile exports from Guatemala to the US has increased 10 percent from 2020 to 2023.4 While manufacturing in the country costs around 5 to 10 percent more than in Vietnam, shipping times are around 3x faster.

Turkey’s share of global textile production has doubled over the past two decades. In 2023, its share of textile and apparel exports to Europe reached 6 percent, surpassing Vietnam.

More than 25 percent of European brands listed Turkey as a crucial sourcing location, according to supply chain compliance company Qima. Brands such as Inditex, H&M, Boohoo and Asos have large sourcing footprints in Turkey.

Advantages include increased supply chain traceability and reduced order-to-fulfilment times, from 150 to 170 days in Asia-Pacific to under 50 days in Turkey, with an average of 7 days in transit.

How should executives respond to these shifts?

1. Regularly assess and optimise sourcing footprint

Regularly perform footprint assessments to identify priority regions for reconfiguration based on manufacturing costs and capabilities, considering potential supply chain disruptions that may impact both (e.g. conflicts, climate change).

Leverage analytics to examine cost breakdowns, improve unit costs and conceive more competitive sourcing processes with both existing and new vendors. This may require detailed supplier information to model costs based on a range of inputs and trade agreements.

Assess cost competitiveness on a net margin basis when making sourcing decisions, taking into account not just input costs but final margin and cash benefits from faster speed-to-market and increased supply chain flexibility.

Develop an understanding of supply chain disruptions across the footprint, actively managing and minimising the implications on their operations, such as cost and speed-to-market.

2. Develop strategic relationships with manufacturers and suppliers

Rethink the approach to manufacturers and suppliers, with an emphasis on developing long-term strategic partnerships to increase the efficiency and resilience of supply chains. Historically, fashion brands and suppliers have been more cautious in making joint investments compared to other industries, given the highly competitive nature of the apparel market. However, the increased disruption and volatility in brands’ sourcing footprints requires more effective and closer collaboration to ensure efficient operations.

Adopt digital solutions to enable efficiency and collaboration. To unlock the full value of these tools, fashion brands and manufacturers will need to not only embrace digital tools across their value chain, but also prioritise process redesign, data quality enhancement and the integration of planning systems to provide visibility for all parties across the value chain.

3. Shape trade flows with industry stakeholders

Proactively shape the future of apparel and textile trade flows by engaging manufacturers, regulators and sustainability bodies to align on industry targets and co-invest in decarbonisation projects at scale.

Work closely with manufacturers and upstream suppliers to achieve sustainability goals and reduce apparel emissions. This remains a competitive imperative for suppliers and fashion brands are unable tackle these issues alone.

Adopt a collaborative planning process to align on short- and long-term business objectives, mutual targets and strategic plans, which can formalise industry affiliations and arrangements. Multiple brands, suppliers and regulators can also partner to launch large-scale sourcing excellence programmes.

This article first appeared in The State of Fashion 2025, an in-depth report on the global fashion industry, co-published by BoF and McKinsey & Company.

{kind=link}